Oil Shocks, Missiles, and Market Crossroads: Why This Week May Redefine Risk

The sudden escalation between Israel and Iran over the weekend has thrust global markets into a new state of uncertainty with oil shocks. Missiles and drones were exchanged. Civilian casualties are mounting. And oil prices are once again the battlefield of geopolitical risk.

While headlines focused on the destruction, markets immediately priced in the possibility of prolonged disruption. Brent crude opened at $78.32 per barrel before retracing to $75.30 — still up nearly 2%. Bloomberg Intelligence now sees WTI potentially spiking to $125, while BCA Research has raised the odds of a historic oil supply disruption to 50%.

But the true implications stretch far beyond oil. Bitcoin remains firm above $100,000, gold is charging toward all-time highs at $3,500, and the U.S. dollar has rallied against most majors. The market is whispering something deeper — and investors should listen closely.

🔎 What Just Happened?

Israel announced its military is now targeting Iran’s regime itself — a step well beyond tit-for-tat retaliation. The U.S. was informed but did not participate. Oil infrastructure has reportedly been damaged. Iran is expected to retaliate soon, and global risk assets are feeling the heat.

Meanwhile, President Trump continues to stand firmly behind Israel, with language that suggests he is prepared for — if not welcoming — a prolonged conflict. This is no longer a regional spat. It’s an economic flashpoint with global implications.

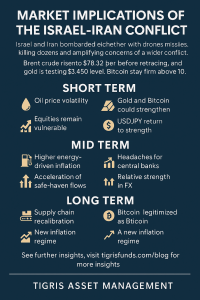

📊 Short-Term Market Implications

- Oil volatility returns. Traders are repositioning rapidly. Brent and WTI are already higher, and risk premiums are back in the energy complex.

- Gold and Bitcoin shine. As traditional safe-havens respond to heightened uncertainty, gold is testing $3,450 and looks poised to retest all-time highs. Bitcoin has surprisingly held above $100,000, signaling a maturing narrative as a non-sovereign hedge during geopolitical stress.

- Equities tread carefully. U.S. futures initially sold off, but buyers returned. This tug-of-war between fear and liquidity continues, but geopolitical shocks could derail fragile momentum.

- USDJPY strength. The dollar remains firm against the yen (144.50), as Japanese investors pull capital home and prepare for domestic policy shifts.

⏳ Mid-Term Risks and Repricing

- Energy-driven inflation risks. Should oil break through $100, the disinflationary narrative driving recent Fed dovishness may be short-lived. Higher energy costs could reverse the recent CPI downtrend.

- Central bank headaches. This week alone features decisions from the Fed, ECB, BoJ, BoE, SNB, and China’s PBoC. A sustained energy shock complicates rate path expectations — especially for central banks aiming to cut in Q3.

- Safe-haven flows accelerate. Continued escalation will boost flows into gold, USD, and yes — Bitcoin, as its correlation to geopolitical risk becomes more favorable than equity beta.

- FX winners emerge. In Asia, the TWD continues to gain, and currencies with strong fundamentals and current account surpluses could outperform if global capital seeks safety and valuation.

🌍 Long-Term Strategic Implications

- Supply chain recalibration. If Middle East shipping lanes become compromised, global trade costs rise. This is especially critical for energy-intensive industries and emerging markets reliant on imported oil.

- Bitcoin legitimized. With fiat currencies tied to the monetary and geopolitical strategies of nation-states, the market may increasingly treat Bitcoin as digital gold — particularly in emerging economies facing currency volatility or capital controls.

- A new inflation regime? The deflationary world of the past decade was built on cheap energy and global trade. If oil supply becomes structurally constrained, a stagflation-lite world may re-emerge, where growth is capped and inflation sticky.

🧭 What to Watch This Week

- Mon: China Retail Sales, Industrial Production

- Tue: Bank of Japan rate decision

- Thu: FOMC, SNB, BoE decisions

- Fri: China Loan Prime Rate, Japan and Hong Kong CPI

- Wild Card: Further retaliation from Iran or proxy actors — any strikes on Saudi, UAE, or regional pipelines would be a gamechanger.

Final Takeaway

This is not a drill. The market has been lulled into a false sense of calm amid falling inflation and dovish central banks. The Israel-Iran conflict is a stark reminder that geopolitics still matters, and energy security is not guaranteed.

In such an environment, investors must stay agile. The short-term may be volatile, but the mid- to long-term winners will be those who can navigate between policy pivots, risk repricing, and a redefined macro regime where Bitcoin, energy, and geopolitics intersect.

📚 For a deeper look into global risk, commodities, and crypto as macro hedges, read our full archive: Tigris Funds Insights

No Comments